If you live in Spain and have financial interests in other countries, you have likely heard whispers about a strict tax requirement for expats. The document in question is form 720 (Modelo 720), an informative tax return designed to tell the Spanish Tax Agency (Agencia Tributaria) about your assets and rights located outside of Spain.

While it does not require you to pay any taxes at the time of submission, failing to file this foreign assets declaration—or filing it incorrectly—can lead to penalties. Fortunately, recent legal changes have made the consequences far less severe than they used to be. Here is exactly what you need to know to stay compliant and avoid unnecessary headaches.

What is form 720 and who must file it?

Any tax resident in Spain—whether a Spanish national, an expat, or an entity—must submit this document if they hold significant assets abroad. This includes individuals, authorized representatives, and beneficiaries who hold powers of disposition over foreign wealth.

The core objective of this declaration of foreign assets is purely informative. The Spanish government uses this data to prevent tax fraud and ensure that any income generated from these assets is properly reported on your annual Income Tax Return (Declaración de la Renta).

The €50,000 threshold rule

You are only required to file this document if the value of your assets in any of the three specific asset groups exceeds €50,000. If the total value within a single group is €49,000, you do not need to report that group. However, if one group exceeds the limit, you must report all assets within that specific category, regardless of their individual value.

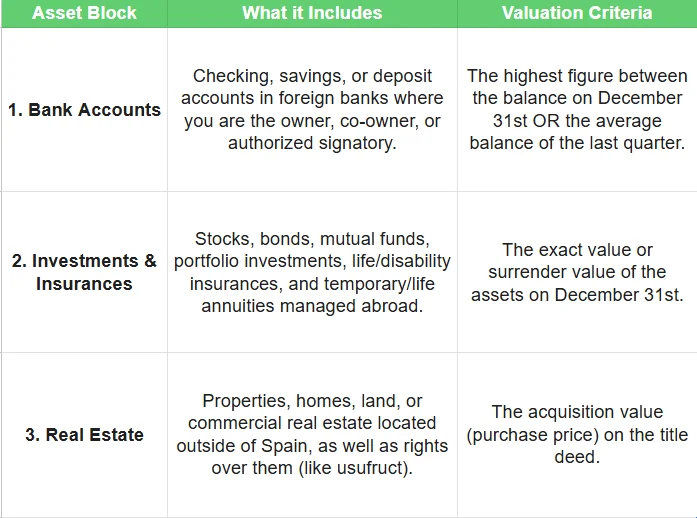

What to include in your foreign assets declaration

The Tax Agency divides foreign assets into three distinct blocks. You must calculate the value of your assets within each block separately as of December 31st of the reporting year.

Important exclusions

Keep in mind that cryptocurrencies are no longer reported on this document. As of recently, virtual currencies held abroad must be reported on a separate, specific document known as Modelo 721.

How and when to submit form 720

The filing period opens every year on January 1st and closes strictly on March 31st. You report the assets held during the previous calendar year. For example, any foreign wealth you held in 2025 must be declared by the end of March in 2026.

Submission process

Spain requires this form to be filed entirely online. You cannot submit a paper copy. To access the electronic portal, you will need one of the following digital identification methods:

- A valid Digital Certificate (Certificado Digital)

- An electronic DNI (DNIe)

- The Cl@ve PIN system

Once logged into the Tax Agency website, you will manually input the details for each asset, including the country code, asset type, and valuation. If you use tax software, you can also import a pre-generated file. Because the platform can be highly technical and requires specific sub-codes, many taxpayers rely on an authorized representative or tax advisor to submit the document on their behalf.

Subsequent filings and updated penalties

One of the biggest reliefs for expats is that you do not necessarily have to file this document every single year.

When to file again

Once you have submitted your first declaration, you only need to file again in future years if:

- The total value of an already declared block increases by €20,000 or more compared to your last submission.

- You sell, cancel, or relinquish ownership of an asset you previously declared.

The end of disproportionate fines

For years, this tax obligation was infamous for its draconian fines. However, a landmark 2022 ruling by the Court of Justice of the European Union (CJEU) declared the old penalty system illegal and contrary to the free movement of capital.

Spain subsequently modified the law. Today, the terrifying penalties of €10,000 minimums or 150% fines are gone. Mistakes, late filings, or omissions are now penalized under Spain’s standard General Tax Law. Typically, submitting the document voluntarily after the deadline without a prior requirement from the tax office carries a standard, manageable penalty (usually €20 per data set, capped or reduced for voluntary compliance), making the process far less stressful.

FAQs

Do I have to file this document if I move to Spain mid-year?

It depends on your tax residency status. If you lived in Spain for more than 183 days during the calendar year, you are considered a tax resident and must evaluate if your foreign assets exceed the €50,000 threshold across the three asset blocks.

What exchange rate should I use for assets not in Euros?

You must convert the value of your foreign assets into Euros using the official exchange rate published by the European Central Bank or the Bank of Spain as of December 31st of the reporting year.

Are pensions held in another country included in this declaration?

Standard state pensions or private pension plans that cannot be redeemed as a lump sum before retirement generally do not need to be declared. However, if the pension is structured as a life insurance policy or an annuity that can be surrendered, it must be reported in Block 2.

Handling cross-border assets and understanding exactly what the Spanish Tax Agency expects from you can be incredibly overwhelming. A simple mistake in a sub-code or valuation can lead to unnecessary administrative letters.

If you need personalized assistance, at Entre Trámites we offer management and tax advisory services for freelancers and SMEs. You can contact us through this contact form for us to call you, or if you prefer, you can schedule a free consultation or write to us on WhatsApp.