Form 714 is the official return for Spain’s Wealth Tax (Impuesto sobre el Patrimonio). It taxes your net worth (assets minus deductible debts) as of 31 December of the relevant tax year, applying the rules in Law 19/1991.

If you need to file Form 714, you must do it online using the Spanish Tax Agency’s web form (Modelo 714) through the “Servicio tramitación de declaración de Patrimonio”.

This guide explains who must file, what information you need, and the steps to submit Form 714 online without missing key checks.

Who must file Form 714 for Wealth Tax?

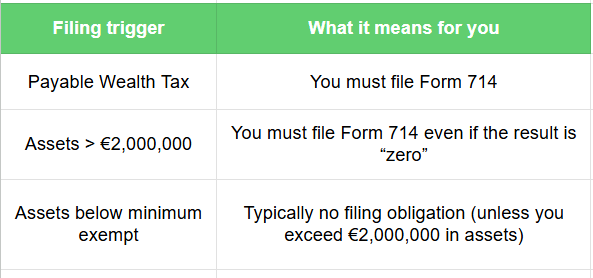

You are required to file Form 714 if you meet either of these conditions:

- Your Wealth Tax liability results payable (after applying any deductions/bonifications that apply to you).

- Even if no tax is payable, the value of your assets and rights exceeds €2,000,000 (calculated under Wealth Tax rules and without subtracting debts for this specific threshold test).

Spain’s general minimum exempt threshold is €700,000, but Autonomous Communities can set different thresholds for residents in their territory.

Quick checklist

Important: Wealth Tax is a “ceded” tax—regions can apply their own scales and bonifications, which can materially change the final amount. The Spanish Tax Agency publishes summaries of regional bonifications for each campaign.

When is Form 714 filed?

The filing period for Form 714 is the same as the annual Personal Income Tax (IRPF) return each year, regardless of whether the result is payable or negative. (Agencia Tributaria)

If you choose direct debit, the direct-debit deadline is also the same as the IRPF direct-debit deadline.

You can always confirm the current campaign dates on the Spanish Tax Agency’s Wealth Tax page (Impuesto sobre el Patrimonio).

What you need before you start

To complete Form 714 smoothly, prepare:

- Identification method to access the online service:

- Electronic certificate, Cl@ve Móvil/Cl@ve PIN, reference number, or eIDAS.

- A list of your assets and rights as of 31 December:

- Real estate, bank accounts, investments, shares, life insurance savings, vehicles/boats (where applicable), business participations, etc.

- Your deductible debts and liabilities (e.g., certain mortgages/loans, if deductible under Wealth Tax rules)

- Supporting documentation to justify valuation figures (statements, deeds, certificates)

If you don’t yet have digital access, an internal help article you can link here is your guide to getting a Digital Certificate (tag: Digital Certificate).

Form 714 online: step-by-step submission

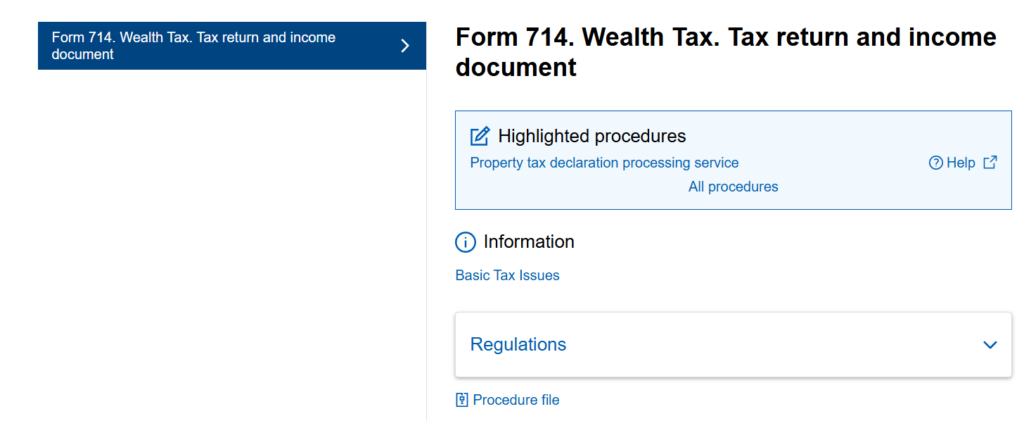

Step 1 — Access the official Wealth Tax filing service

Go to the Spanish Tax Agency’s procedure page for Modelo 714 and open “Servicio tramitación de declaración de Patrimonio”.

Because the filing is electronic only, you cannot submit Form 714 on paper.

Step 2 — Identify yourself

Choose one of the accepted methods:

- Electronic certificate

- Cl@ve Móvil (includes Cl@ve PIN)

- Reference number

- eIDAS

Step 3 — Fill in your personal and tax data

Confirm:

- Tax year

- Tax residence situation (residents are typically taxed on worldwide assets; non-residents only on Spanish-situated assets, with important nuances)

- Autonomous Community of residence (if applicable)

Step 4 — Declare assets and rights

Form 714 is organised by asset categories. The key is to enter each item in the correct section and apply the correct valuation rule for that asset type.

Practical tip: Keep your entries consistent with how each asset is legally held (sole owner, joint ownership, marital property regime, etc.). This avoids mismatches and future requests for clarification.

Step 5 — Declare deductible debts

Enter debts and obligations that are deductible under Wealth Tax rules, so the system can compute your net worth.

Step 6 — Review the summary and calculate the result

Once you complete the asset and debt sections, the form produces a summary and calculates the tax outcome (payable or zero/negative). This is where regional rules can matter, because regions may apply bonifications.

Step 7 — Choose payment method (if payable) and submit

If the return is payable:

- You can usually pay via direct debit (within the direct-debit deadline), or other allowed payment methods, depending on the campaign setup.

- Submit the form online and save the receipt/proof of filing.

Common mistakes when filing Form 714 online

- Forgetting the €2,000,000 assets threshold (you may need to file even if you owe nothing).

- Using “approximate” values without documentation (risky if the Tax Agency requests support).

- Missing region-specific rules (bonifications and thresholds can change outcomes).

- Waiting until the last week and then struggling with identification or technical access (especially if your certificate or Cl@ve is not ready).

If you’re not sure whether you must file Form 714, or you want to confirm valuations and apply the correct exemptions/bonifications, it’s worth doing a quick pre-review before submitting. Wealth Tax returns are detail-heavy, and correcting errors later can be time-consuming.

Frequently Asked Questions (FAQs)

Do I have to file Form 714 if I don’t have Wealth Tax to pay?

Yes, if the value of your assets and rights exceeds €2,000,000, even if the result is zero.

When is Form 714 filed in Spain?

The filing period is the same as the annual IRPF (income tax) filing period each year.

Can Form 714 be submitted on paper?

No. Wealth Tax returns must be filed electronically using the online Modelo 714 service.

Filing Form 714 is mainly about organisation: knowing whether you must file, gathering the right documentation, and entering assets and debts correctly in the online form. If you handle it properly from the start, you reduce the risk of follow-ups and keep your tax position clean.

If you need personalized assistance, at Entre Trámites we offer management and tax advisory services for freelancers and SMEs. You can contact us through this contact form for us to call you, or if you prefer, you can schedule a free consultation or write to us on WhatsApp.