Expanding your foreign business into the Spanish market is an exciting growth opportunity, but it often comes with a major legal fear. Many foreign companies absolutely panic about operating locally and accidentally triggering a permanent establishment in Spain. If you cross this invisible line, your business is suddenly forced into the local corporate tax system, meaning you have to pay taxes on the income generated within the country.

If you are directing operations from the US, the UK, or anywhere else abroad, understanding this concept is crucial. In 2026, the Spanish tax authorities are aggressively cracking down on foreign entities operating under the radar. Let’s break down exactly what this legal concept means, the red flags to watch out for, and how to keep your operations compliant and tax-efficient without triggering unexpected audits.

What exactly constitutes a permanent establishment in Spain?

In local tax law, an Establecimiento Permanente (Permanent Establishment or PE) occurs when a foreign entity has a continuous or habitual presence in the country to carry out economic activities. When this happens, your business is treated almost like a local resident company. You become liable for the Impuesto sobre Sociedades (Corporate Tax), which currently sits at a standard rate of 25% on the net income attributable to your Spanish operations.

According to Spanish legislation and standard OECD treaties, you generally trigger this status in one of two main ways. First, through a fixed place of business. Second, through a dependent agent acting on behalf of your company.

The Fixed Place of Business

If you lease a physical space to conduct your core business operations, you are waving a red flag. This includes management offices, factories, workshops, warehouses (in certain commercial contexts), or a registered Sucursal (a formal branch office). Even a long-term construction or installation project that lasts longer than the timeframe specified in your country’s double taxation treaty (often 6 to 12 months) can create a PE.

The Dependent Agent

You do not need a physical office to get caught in the tax net. If you hire a person in Spain who habitually exercises the authority to negotiate and conclude binding contracts in the name of your foreign company, they are considered a dependent agent. Because they are generating direct revenue for you on Spanish soil, the government views this as a taxable presence.

How Companies Accidentally Fall into the Tax Net

Many modern businesses trigger a permanent establishment in Spain completely by accident. The rise of remote work and borderless sales teams has blurred the lines of international taxation. Here are the most common ways foreign companies unknowingly cross the line.

The Remote Executive Risk

Allowing a C-suite executive or a high-level sales director to live in Spain as a digital nomad can be dangerous for your company. If that employee is making strategic management decisions or signing large client contracts from their laptop in Valencia, the tax office may argue that your company’s management is effectively taking place in Spain.

Server and Digital Presence

For tech companies, the physical location of servers can sometimes be scrutinized. While simply having a localized website does not create a PE, owning and operating dedicated server infrastructure within Spanish territory that runs your core business services might cross the threshold.

Independent vs. Dependent Contractors

Hiring freelancers (Autónomos – registered self-employed professionals) is generally safe, provided they act independently and offer their services to multiple clients. However, if you hire an independent contractor but they only work for you, use your company email, and have the power to sign deals on your behalf, the authorities will reclassify them as a dependent agent.

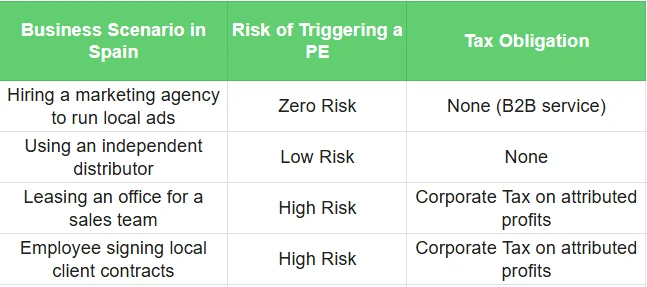

To give you a clear visual, here is a quick breakdown of how different scenarios impact your corporate tax obligations:

Transfer Pricing: The Top Inspection Priority

If you knowingly or accidentally establish a PE, paying the 25% corporate tax is only half the battle. Your relationship with Hacienda (the Spanish Tax Agency) becomes incredibly complex due to Precios de Transferencia (Transfer Pricing).

Transfer pricing refers to the rules and methods used to price transactions between your foreign head office and your Spanish branch. For example, if your US parent company charges your Spanish PE for “management fees” or “software licensing,” the prices for those internal services must be strictly at market value (the arm’s length principle).

In 2026, transfer pricing is an absolute priority for tax inspectors. Foreign companies often try to artificially shift profits out of Spain by overcharging their local branch for internal services, thereby lowering the taxable profit locally. Hacienda actively hunts for these discrepancies. If they audit you and find that your internal pricing does not reflect true market conditions, you will face severe penalties, double taxation issues, and hefty interest charges on the unpaid tax.

Protecting Your Foreign Business

The best way to avoid a permanent establishment in Spain is through strict operational boundaries. If you hire staff locally, limit their authority. Do not allow remote workers to sign binding agreements or negotiate final pricing. Use independent distributors who manage their own business risk, and never lease a permanent commercial space unless you are fully prepared to register a subsidiary or a formal branch.

If you are unsure about your current setup, it is vital to consult with a specialized cross-border tax advisor. Taking proactive steps today will protect your company from crippling tax liabilities and intense audits tomorrow.

Frequently Asked Questions (FAQs)

What happens if I accidentally create a permanent establishment in Spain?

If the Spanish Tax Agency determines you have an undeclared PE, they will demand back taxes on the corporate income attributed to Spain for the years you operated illegally. You will also face significant penalty surcharges and late payment interest.

Can an employee working from home in Spain trigger corporate taxes for my company?

Yes, it is possible. If the employee simply performs back-office, preparatory, or auxiliary tasks, you are generally safe. However, if they actively negotiate contracts, close sales, or perform core revenue-generating management duties from their home office, they act as a dependent agent, which triggers the tax.

How does Hacienda find out about foreign companies operating locally?

The Spanish tax authorities use automated data matching. They track the social security registrations of your employees, monitor local bank transactions, review lease agreements for commercial properties, and exchange information with other European tax authorities. They also frequently audit companies with unusually high cross-border invoicing.

If you need personalized assistance, at Entre Trámites we offer management and tax advisory services for freelancers and SMEs. You can contact us through this contact form for us to call you, or if you prefer, you can schedule a free consultation or write to us on WhatsApp.