What is the Beckham Law? It is the common name for Spain’s Special tax regime for workers posted to Spanish territory, regulated under Article 93 of the Spanish Personal Income Tax Law (Law 35/2006).

This regime allows certain foreign workers who move to Spain for employment reasons to be taxed under non-resident income tax rules, even though they become Spanish tax residents.

In practical terms, it means you can benefit from a flat tax rate on employment income instead of Spain’s progressive income tax scale.

Below, you’ll find a clear explanation of what is the Beckham Law, who qualifies, how it works, and how to apply correctly.

What is the Beckham Law and who can apply?

The Beckham Law applies to individuals who move to Spain as a result of:

- An employment contract with a Spanish employer

- A transfer from a foreign company to a Spanish entity

- Being appointed as a company director (with certain shareholding limits)

- Performing entrepreneurial or highly qualified professional activities under specific conditions introduced by the Startup Law (Law 28/2022)

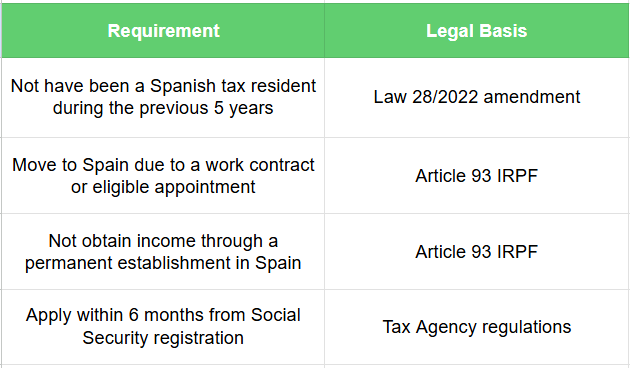

To qualify, you must meet these legal requirements:

The reduction from 10 to 5 years of prior non-residence was introduced by the Startup Law to make Spain more competitive in attracting international talent.

How does taxation work under the Beckham Law?

Understanding what is the Beckham Law requires looking at how income is taxed.

Under this regime:

- Employment income up to €600,000 per year is taxed at 24%

- Income exceeding €600,000 is taxed at 47%

- Only Spanish-source income is generally taxed (with some exceptions)

Unlike ordinary tax residents, you are taxed under Non-Resident Income Tax (IRNR) rules, even though you are considered resident for other purposes.

Key advantages

- Flat 24% rate instead of progressive IRPF rates (which can exceed 45% depending on the region)

- No taxation on worldwide income (except employment income)

- Wealth Tax applies only to assets located in Spain

- No obligation to file Form 720 (assets abroad declaration)

This makes the regime particularly attractive for executives, tech professionals, and internationally mobile workers.

Who cannot apply?

The Beckham Law does not apply to:

- Self-employed individuals operating through a permanent establishment

- Professional athletes (excluded under the reform of 2010)

- Directors who hold more than 25% of company shares (unless specific Startup Law exceptions apply)

If you are planning to work as a freelancer in Spain, this regime generally does not apply to you.

How long does the Beckham Law last?

The regime applies during:

- The year of arrival in Spain, and

- The following five tax years

In total, you can benefit for up to six years.

It does not extend automatically beyond this period.

How to apply step by step

Applying correctly is essential. If you miss the deadline, you lose the right to opt for the regime.

Step 1: Register with Social Security

You must first be registered as an employee in Spain.

Step 2: Submit Form 149

The application must be filed within six months from your Social Security registration date.

Form 149 is submitted to the Spanish Tax Agency electronically.

You must provide:

- Passport

- NIE

- Employment contract

- Social Security number

- Company certification

Step 3: Annual filing using Form 151

If approved, you will file your annual tax return using Form 151, not the standard Form 100.

The Tax Agency will issue a resolution confirming acceptance of the regime.

Disadvantages to consider

Although attractive, the regime has limitations:

- Limited access to double taxation treaties

- No application of standard IRPF reductions and family allowances

- Certain exemptions (such as severance pay exemptions) may not apply

- No deduction of typical personal allowances available under ordinary IRPF

Before applying, it is essential to compare scenarios.

For some professionals with moderate income, the standard progressive regime may actually result in lower taxation.

Practical example

If you earn €120,000 per year as an executive in Madrid:

- Under the Beckham Law → 24% flat rate

- Under ordinary IRPF → progressive scale (which may exceed 40%)

The difference can be significant, especially during the first years of relocation.

However, if your income is below €50,000, the tax saving may be smaller.

Understanding what is the Beckham Law is not just about knowing the 24% rate. It is about analysing whether you meet the requirements and whether the regime truly benefits your personal tax situation.

Frequently Asked Questions (FAQs)

What is the Beckham Law in Spain?

It is a special tax regime allowing certain foreign workers to pay a flat 24% rate on employment income instead of progressive IRPF rates.

How long can I benefit from the Beckham Law?

The regime applies for six tax years: the year of arrival plus five additional years.

Can freelancers apply for the Beckham Law?

Generally no, if they operate through a permanent establishment in Spain. The regime mainly applies to employees and certain directors.

If you are relocating to Spain for work, understanding what is the Beckham Law can make a substantial difference in your tax planning. Proper advice ensures you apply on time and choose the regime that truly benefits you.

If you need personalized assistance, at Entre Trámites we offer management and tax advisory services for freelancers and SMEs. You can contact us through this contact form for us to call you, or if you prefer, you can schedule a free consultation or write to us on WhatsApp.